The global race to build Artificial Intelligence has sparked one of the largest investment cycles in modern history. With projections of $1.5 trillion being poured into AI by 2025, the excitement is understandable-AI can potentially lift global productivity by more than 10%, making this investment look small relative to a $100 trillion world economy. But as Rohit Tripathi explains, the problem isn’t AI itself. The real danger lies in the financial engineering happening behind the scenes, particularly through Special Purpose Vehicles (SPVs) that hide massive debt and artificially inflate valuations.

The New Circular Economy of AI

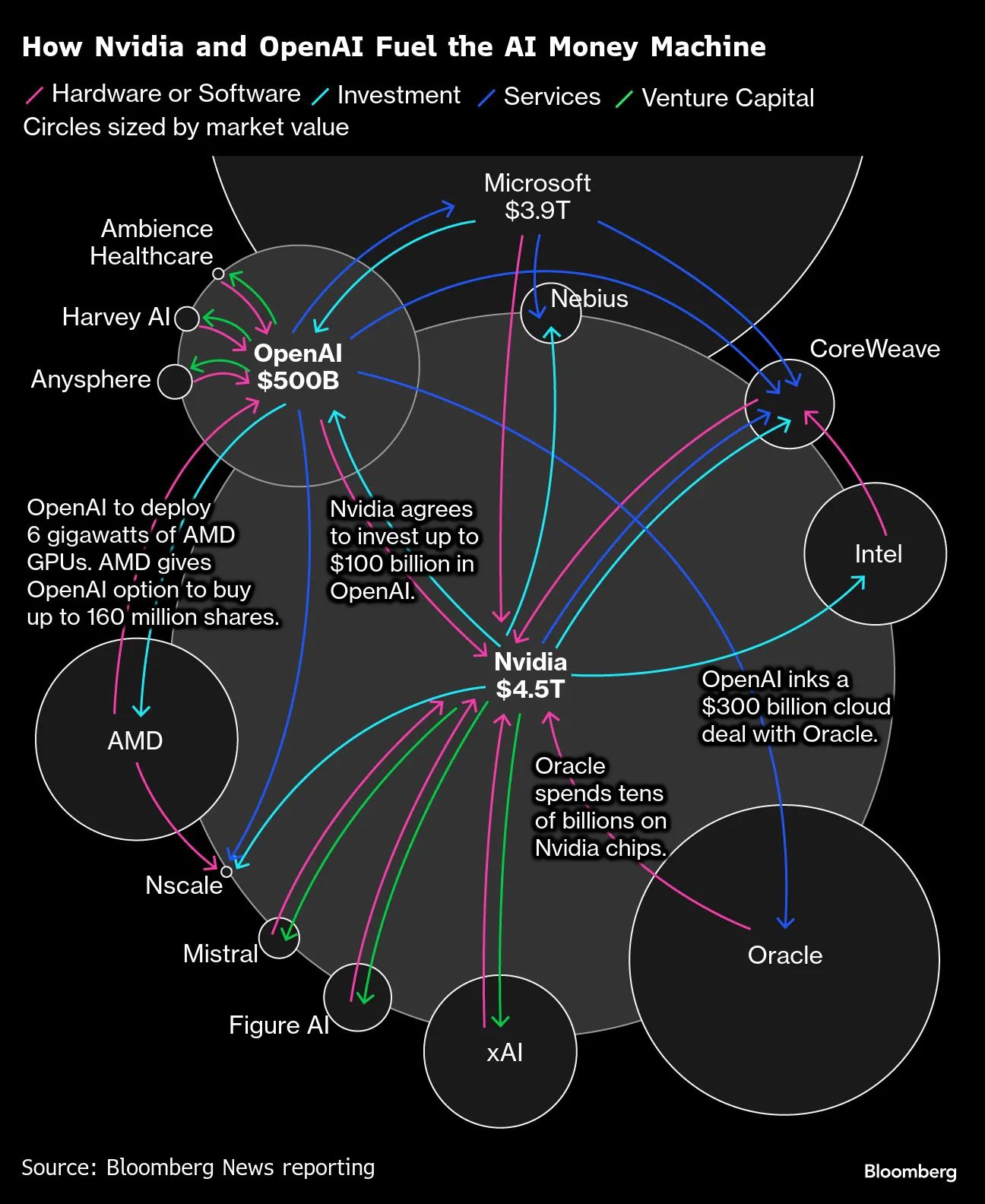

Tripathi begins by showing how companies like Nvidia, OpenAI, AMD, Coreweave, and others are locked in a circular financing loop.

OpenAI needs GPUs but doesn’t have the cash-its estimated daily loss is around $15 million. Nvidia “invests” billions into OpenAI, and OpenAI immediately uses that money to buy Nvidia’s chips. This inflates valuations for both sides:

- OpenAI’s books show fresh inflows and higher valuations.

- Nvidia’s revenue looks stronger-even though the money originated from Nvidia itself.

This circular system creates a false sense of demand, inflates chip sales, and pushes stock prices higher without underlying real profitability.

Tripathi also highlights through his video how AMD entered this game through warrants, giving OpenAI the right to buy AMD shares at $0.01-a near-zero price-allowing OpenAI to show “investment capability” without spending real money. The stock pops, OpenAI books gains, and that money is used to buy AMD chips. The loop continues.

Image Source – https://www.bloomberg.com/news/features/2025-10-07/openai-s-nvidia-amd-deals-boost-1-trillion-ai-boom-with-circular-deals

Coreweave and the Hidden Interlocks

Companies like Coreweave add another layer of complexity. Coreweave builds AI data centers powered by Nvidia chips. Nvidia is also an investor in Coreweave. At the same time, Coreweave sells cloud services to Nvidia and OpenAI.

So Nvidia invests in a company that buys Nvidia chips, and Nvidia becomes that company’s major customer. Each announcement of a deal sends both stocks soaring-another engineered boost, not reflective of organic demand.

Geopolitics Creates Fake Shortages-And Bigger Bubbles

US restrictions on selling advanced chips to China created a “shortage premium,” but companies quickly discovered legal loopholes. Tripathi highlights how European firms such as Nebius buy Nvidia’s chips legally and then rent their computing power to Chinese firms at inflated rates.

And Nvidia has also invested in Nebius.

Every geopolitical twist ends up benefiting the same players-while inflating chip prices further.

SPVs: The Heart of the Debt-Hiding Mechanism

The most dangerous element in Tripathi’s breakdown is the rise of SPVs (Special Purpose Vehicles)-shell companies used to hide debt.

How SPVs hide the truth

Tripathi uses Elon Musk’s xAI and its “Colossus” supercomputer project as the clearest example:

- xAI needs $20 billion for GPUs.

- If xAI borrowed directly, its balance sheet would collapse.

- So Musk created an SPV that takes $12.5B debt and $7.5B equity.

- The SPV buys Nvidia GPUs.

- xAI rents those GPUs for 5 years and records only “rental expense”-not debt.

The result?

xAI looks financially healthy.

The debt exists, but hidden inside the SPV.

And Nvidia ends up being an investor in the same SPV buying Nvidia’s chips.

Tripathi notes that Meta and Microsoft are also using similar structures. This creates a shadow capex cycle-massive hidden leverage behind depreciating hardware.

Why This Is More Dangerous Than 2008 or Dot-Com

Tripathi draws parallels to both past crises:

- Like 2008, excessive leverage is building-but this time around GPUs, which are guaranteed to depreciate.

- Like Dot-Com, companies are slapping “AI” on everything-AI refrigerators, AI toothbrushes-manufacturing hype.

GPU rental rates have already fallen 75%, showing early cracks in the model.

If AI revenue grows slowly or plateaus, SPVs will collapse under debt, pulling lenders, pension funds, insurers, and tech companies into a systemic crisis.

Apple & Google: The Only Sane Players

Tripathi points out that two giants-Apple and Google-are almost entirely absent from this debt-fuelled bubble.

Apple:

- Avoided massive AI data-center capex

- Focuses on local compute using in-house chips

- Has no dependency on Nvidia

Google:

- Uses its own TPU hardware

- Funds AI from internal cash flows

- Already monetizes AI via Search, Gmail, YouTube

While the market chases hype, these two companies quietly build AI sustainably.

When Will the Bubble Burst?

Tripathi predicts the next major crash could align with the market’s 8-year cycle, placing the risk window around 2028. But he also notes that bubbles burst precisely when no one expects them-making this timeline only directional, not certain.

Final Thoughts

Rohit Tripathi emphasizes repeatedly: AI is not the problem.

The bubble is being formed by hidden debt, circular financing, SPVs, and unrealistic expectations-not by the technology itself.

Investors must understand what they’re truly buying into.

{kind=link}