When investors evaluate a company, they often get distracted by headlines.

For Netflix, those headlines are usually about hit shows like Squid Game and Stranger Things, live sports, password-sharing crackdowns, or the rapid growth of advertising.

While these developments attract attention, they don’t necessarily reveal whether the underlying business is truly strong.

To assess Netflix’s fundamental strength, we need to look beyond the headlines and focus on the numbers that drive the company.

A fundamentally strong business is typically characterized by consistent revenue growth, strong profitability, healthy cash generation, a solid balance sheet, efficient use of capital, and a clear path for future growth.

Let us now break down the numbers and understand the complete fundamentals of the company and get our questions answered.

Revenue Growth: Is The Business Still Expanding?

Revenue represents the total amount of money Netflix collects from customers before any expenses are deducted.

Netflix’s revenue has grown steadily over the past several years. The company generated $29.7 billion in 2021, which increased to $31.6 billion in 2022 and $33.7 billion in 2023.

Growth continued in the following years, with revenue reaching $39 billion in 2024 and approximately $45.2 billion in 2025. Netflix management projects total revenue for 2026 to fall between $50.7 billion and $51.7 billion, which represents 12% to 14% year-over-year growth.

This is particularly impressive because Netflix is no longer a small, fast-growing startup. It already serves hundreds of millions of users around the world, making continued growth much more difficult.

As companies become larger, maintaining high growth rates becomes increasingly challenging. Adding 10% growth to a small business is relatively easy compared to adding 10% growth to a company generating tens of billions of dollars in annual revenue.

Despite its enormous size, Netflix continues to deliver double-digit revenue growth, which is a strong indicator of a healthy and expanding business.

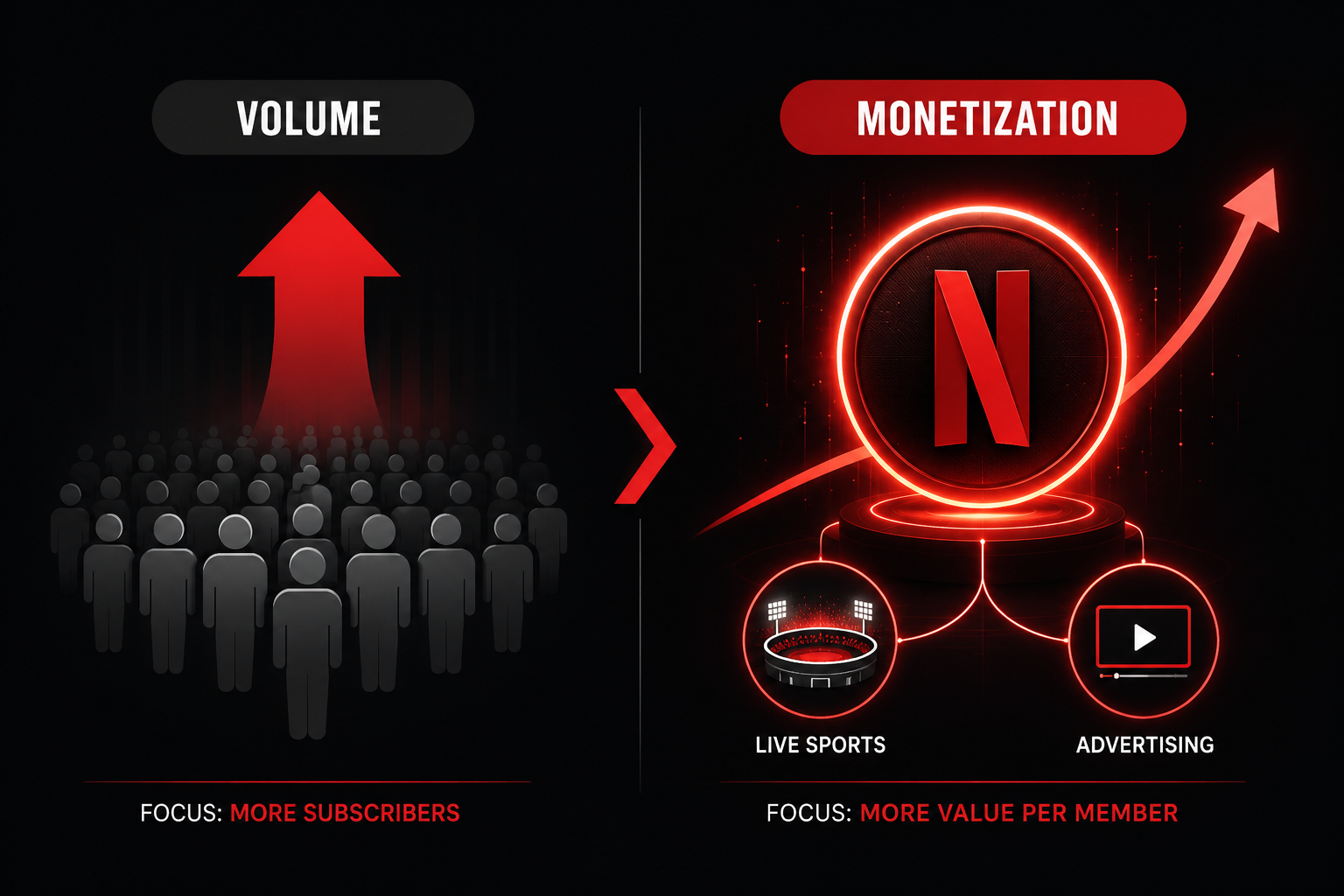

The Average Revenue Per User Shift

While a 12% to 14% growth rate on a massive revenue base is mathematically impressive, investors must analyse the quality of that revenue. Netflix is undergoing a structural shift from “volume-led” growth (simply adding more subscribers) to “monetization-led” growth.

This expansion is increasingly driven by two newer levers: aggressive ad-supported subscription tiers and systemic crackdowns on password sharing. The core question moving forward is no longer just how many people watch Netflix, but how effectively the company can scale its live sports ad inventory (such as NFL games and WWE partnerships) to extract higher Average Revenue Per User (ARPU).

Subscriber Growth: The Engine Behind Revenue

Every dollar of revenue ultimately begins with people paying for a Netflix membership. As of 2025, Netflix has surpassed 300 million paid memberships globally, making it one of the largest subscription-based entertainment platforms in the world.

What makes this achievement particularly notable is that Netflix continues to add subscribers despite operating in an intensely competitive streaming industry. The company competes with major platforms that are investing billions of dollars in content and customer acquisition.

Subscriber growth is important because it directly expands Netflix’s revenue base. Every new member adds recurring monthly revenue, creating a larger foundation for future growth.

Once that subscriber base grows, Netflix can further increase revenue through carefully managed price increases. Existing customers continue paying for the service, while new subscribers join at the updated pricing levels.

As a result, Netflix benefits from two powerful growth drivers simultaneously: a growing number of paying members and higher average revenue per subscriber.

When both of these factors work together, they create a strong and scalable revenue engine that can drive meaningful long-term growth for the business.

However, this subscriber engine faces an undeniable ceiling. In high-revenue, developed regions like North America, Netflix has achieved near-total market saturation. Consequently, the bulk of its future subscriber additions will come from developing markets in the Asia-Pacific and Latin America regions.

While these areas expand the absolute user count, they generate a significantly lower monthly subscription fee.

Furthermore, the massive subscriber surges seen recently were a one-time “sugar rush” resulting from the global password-sharing crackdown. Now that this operational lever has been fully pulled, the platform must find entirely new hooks to keep its subscriber numbers moving upward.

Operating Margin: Is Netflix Keeping More of Every Dollar?

Revenue growth is important, but revenue alone does not determine the strength of a business.

If expenses rise at the same pace as revenue, a company may generate more sales without becoming significantly more profitable. This is why investors pay close attention to operating margin.

Netflix has made remarkable progress in this area over the past several years. Its operating margin improved from 17% in 2022 to 20% in 2023 to 26% in 2024 and in 2025 it is reported as 29.49%.

Management expects operating margin to rise further to approximately 31% in 2026.

This is one of the most impressive indicators of Netflix’s business strength.

To put it into perspective, imagine Netflix generates $100 in revenue. After paying for content, marketing, technology, and operating expenses, the company is expected to keep roughly $29 as operating profit.

Just a few years ago, Netflix was keeping only about $13 out of every $100 generated.

In other words, the company has more than doubled its operating profitability while continuing to grow revenue at a substantial pace.

This improvement demonstrates that Netflix is becoming increasingly efficient as it scales, allowing a larger share of every dollar earned to flow through as profit.

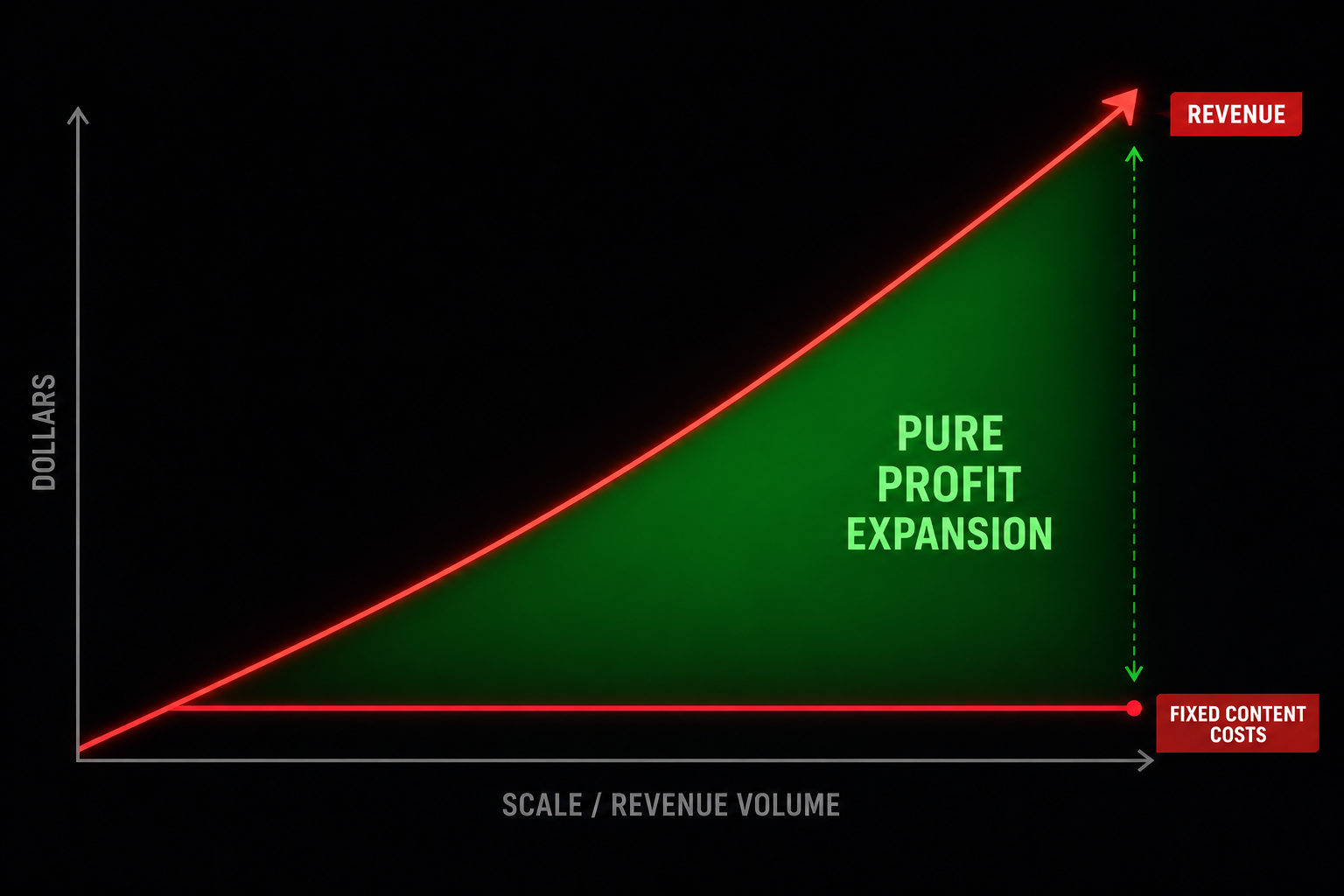

The magic behind this margin expansion from 17% to nearly 30% is a concept known as operating leverage. In the streaming business, content creation expenses are largely fixed; it costs the same amount of capital to produce a hit series whether 10 million or 100 million people stream it.

Because Netflix’s massive global distribution infrastructure is already built and paid for, every single dollar earned from its next 50 million subscribers incurs almost zero incremental cost. This unique business model allows revenue growth to disproportionately compound into pure operating profit.

Earnings Per Share (EPS): The Profit That Matters to Shareholders

EPS measures the amount of profit generated for every share outstanding. A rising EPS generally indicates that shareholders are receiving a larger share of the company’s earnings over time.

Netflix’s EPS has grown dramatically over the past decade.

Today, the company generates several times more earnings per share than it did just five years ago. This reflects not only revenue growth but also improving profitability and operational efficiency.

Why This Matters

- Higher EPS means greater shareholder value.

As earnings per share increase, each share represents a larger claim on Netflix’s profits. - Revenue growth alone is not enough.

A company can increase sales every year while delivering little benefit to shareholders if profits fail to grow at the same pace. - Netflix is growing both revenue and earnings.

The company has successfully converted revenue growth into higher profits, which is a sign of a healthy and well-managed business. - This combination is relatively uncommon.

Many companies can grow revenue, and some can grow profits. Consistently growing both at the same time is far more difficult and often indicates strong business fundamentals.

Key Takeaway

For shareholders, EPS is often more important than total profit because it shows how much value is being created for each share they own. Netflix’s strong EPS growth suggests that the company is not just getting bigger—it is becoming more valuable for its investors as well.

Free Cash Flow: The Most Important Number

Many investors consider Free Cash Flow (FCF) to be one of the most important financial metrics because it shows the actual cash a company generates after covering all of its operating expenses and capital investments.

Think of Free Cash Flow as the money that remains after a company has paid all of its bills and invested in growing the business. This cash can then be used to repay debt, buy back shares, pay dividends, make acquisitions, or simply strengthen the balance sheet.

The turnaround is remarkable. In 2019, Netflix was burning over $3 billion in cash each year to fund its aggressive content expansion. By 2023 and 2024, the company was consistently generating nearly $7 billion in annual free cash flow – a swing of more than $10 billion in just a few years.

Why This Matters

- No longer a cash-burning business: Netflix has moved from consuming cash to generating billions in excess cash every year.

- Reduced dependence on debt: The company no longer needs to borrow heavily to finance its content investments.

- Greater financial flexibility: Strong cash generation allows Netflix to invest in new content, sports, gaming, acquisitions, and shareholder returns without putting pressure on its balance sheet.

- A sign of business maturity: This shift shows that Netflix has evolved from a high-growth, capital-intensive company into a mature business capable of funding its own expansion.

The improvement in Free Cash Flow is arguably one of the strongest indicators of Netflix’s fundamental transformation and long-term financial strength.

Return on Equity (ROE): How Efficient Is Management?

Return on Equity (ROE) measures how efficiently a company’s management uses shareholders’ money to generate profits. It is one of the most widely used metrics for evaluating management performance and capital efficiency.

The formula is simple:

ROE = Net Income ÷ Shareholders’ Equity

A higher ROE generally indicates that a company is generating more profit for every dollar invested by its shareholders.

Netflix’s ROE Performance

Netflix has consistently maintained a Return on Equity of over 30%, placing it among the most efficient large – cap companies in terms of capital allocation.

For perspective:

- 15% – 20% ROE is considered strong for most established businesses.

- Above 25% ROE is generally viewed as excellent.

- Netflix’s 30%+ ROE indicates exceptional management efficiency in converting shareholder capital into earnings.

Example

Imagine shareholders invest $100 into a company. If management generates $30 in net profit from that investment, the company has an ROE of 30%.

Why This Matters

- Shows how efficiently management uses shareholders’ capital.

- Indicates the company’s ability to generate strong profits without requiring excessive investment.

- Reflects disciplined capital allocation and operational efficiency.

- Netflix’s consistently high ROE is another sign that the business has matured into a highly profitable and efficiently managed company.

Source – Netflix financials

The Balance Sheet: Can Netflix Handle Economic Stress?

A balance sheet provides a snapshot of a company’s financial health by showing what it owns (assets), what it owes (liabilities), and the value that belongs to shareholders (equity).

Assets

Netflix’s asset base has grown significantly over the years as the company has expanded its content library and global streaming platform. As of FY2025, Netflix reported total assets of approximately $55.5 billion, including $9 billion in cash and cash equivalents and $9 billion in cash plus short-term investments.

The majority of its assets consist of content assets, technology infrastructure, and other long-term assets that support its streaming business. These large cash reserves provide management with the flexibility to invest in new content, pursue strategic opportunities, and navigate economic slowdowns without putting pressure on the business.

Debt

Debt was once one of the biggest concerns surrounding Netflix. For many years, the company borrowed billions of dollars to finance original content while it was still building its global subscriber base. Investors questioned whether the business could ever generate enough cash to support such aggressive spending.

Today, the situation looks very different. Netflix has transitioned from a cash-burning company to one that consistently generates billions in annual free cash flow. As a result, management is no longer relying on aggressive borrowing to finance growth and has instead shifted its focus toward share repurchases and creating value for shareholders.

Long-Term Debt

Netflix’s long-term debt has remained remarkably stable over the past several years. At the end of 2025, the company reported approximately $13.4 billion in long-term debt, only slightly lower than $14.1 billion in 2023 and well below the rapid debt accumulation seen during its expansion phase. Combined with nearly $9.4 billion in annual free cash flow, this debt level is now much more manageable than it was just a few years ago.

Debt-to-Equity Ratio

Netflix’s capital structure has also improved considerably. At the end of 2025, shareholders’ equity stood at roughly $26.6 billion, while the company’s debt-to-equity ratio was around 0.54x, a much healthier level than during its heavy borrowing years. Lower leverage means Netflix relies less on debt to finance its operations, reducing financial risk and giving the company greater flexibility to invest in future growth opportunities.

If you’re interested in investing in companies like Netflix but aren’t sure how to get started, I’ve created a step-by-step guide explaining how to invest in U.S. stocks from India. You can watch it here: How to Invest in US Stocks

Final Verdict

Based on the financial metrics discussed throughout this article, Netflix appears to be a fundamentally strong company. It exhibits many of the characteristics investors typically look for in a high-quality business: consistent revenue growth, expanding profit margins, rising earnings, robust free cash flow, efficient use of shareholder capital, and a solid balance sheet.

That said, a fundamentally strong company does not automatically make it a fundamentally attractive stock to buy today. The quality of the business and the attractiveness of the investment are two different questions. A great company can still become a poor investment if its stock price already reflects overly optimistic expectations.

Therefore, while Netflix scores highly on business fundamentals, investors should also evaluate its valuation, competitive landscape, future growth prospects, and margin of safety before making an investment decision. Fundamentals tell us how good the business is; valuation determines whether the stock is worth buying at the current price.

In Netflix’s case, the evidence suggests that the business itself is stronger than it has ever been. The next question for investors is not whether Netflix is a quality company – but whether the current market price offers an attractive opportunity.

{kind=link}