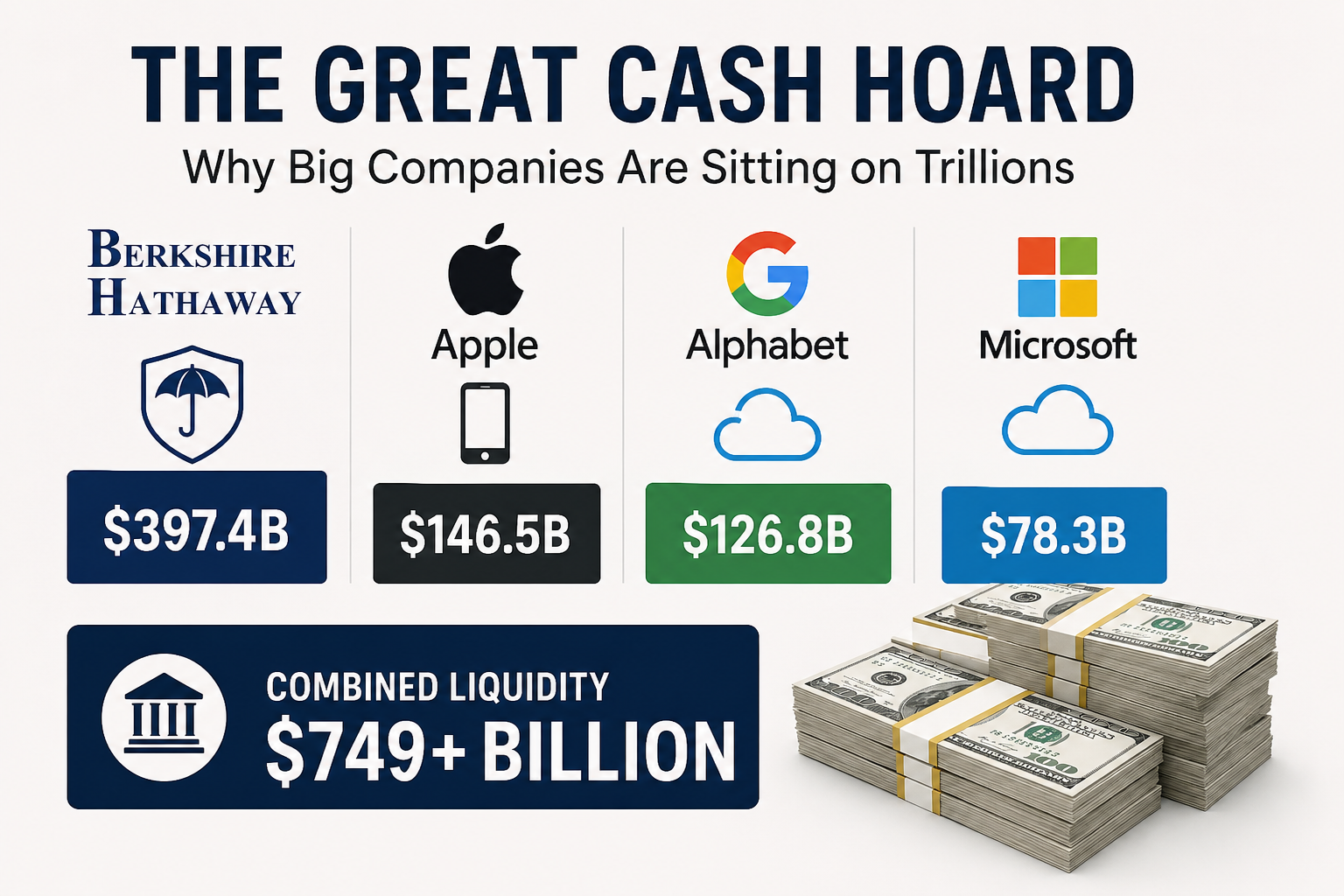

Berkshire Hathaway, Apple, Alphabet, and Microsoft collectively hold more than $750 billion in cash, marketable securities, and short-term investments. At a time when companies are spending heavily on growth, acquisitions, and shareholder returns, these enormous cash balances raise an obvious question: why are some of the world’s most successful businesses still sitting on so much money?

The answer lies in a major shift in the economics of liquidity. In today’s higher-interest-rate environment, cash is no longer a dormant asset. It generates meaningful returns while providing companies with the flexibility to navigate uncertainty and capitalize on future opportunities.

The Corporate Cash Mountain

The scale of corporate cash reserves is staggering.

| Company | Cash & Investments |

| Berkshire Hathaway | $397.4 Billion |

| Apple | $146.5 Billion |

| Alphabet | $126.8 Billion |

| Microsoft | $78.3 Billion |

Combined, these four companies hold more than $749 billion in liquidity. To put that figure into perspective, it exceeds the annual GDP of many countries. More importantly, these balances continue to remain elevated despite aggressive spending on capital expenditure, acquisitions, research and development, and shareholder returns.

The Strategic Divergence: Why Big Cash Is Not Created Equal

Investors often treat corporate cash as one uniform concept. That view is misleading. Berkshire Hathaway, Apple, Alphabet, and Microsoft all hold large cash balances. But the reasons are different.

Berkshire Hathaway’s $397 billion cash position reflects both structure and strategy. The company runs a large insurance business. It requires liquidity to support its insurance float. At the same time, Warren Buffett has increased exposure to Treasury bills while reducing equity exposure. Berkshire now holds more than half of the combined cash across these four companies.

Apple reflects the opposite behavior. The company has tried for years to reduce excess cash. It runs one of the largest buyback programs in corporate history. This includes a $100 billion authorization in 2026. Yet Apple still holds about $146.5 billion in cash and investments. The reason is simple. Its cash generation is extremely strong. It produces more cash than it can distribute.

Alphabet and Microsoft show a different pattern. Their cash is increasingly tied to AI infrastructure investment. Large acquisitions have become harder due to antitrust scrutiny. As a result, capital is moving toward data centers, chips, cloud infrastructure, and energy systems.Microsoft now spends more than $14 billion per quarter on capital expenditure. Alphabet is also scaling its AI investment aggressively. Despite this, both companies continue to maintain large liquidity buffers.

Together, these companies tell different stories. Berkshire is preserving optionality. Apple is outpacing its ability to distribute cash. Alphabet and Microsoft are funding large infrastructure cycles.

The Interest Rate Shift That Changed Everything

For most of the decade following the Global Financial Crisis, holding large cash balances was expensive from a shareholder’s perspective. Short-term government securities yielded close to zero, meaning companies earned almost nothing on billions of dollars sitting in cash.

That environment has changed dramatically.

Three-month U.S. Treasury bills have offered yields of roughly 4%-5% in recent years, turning cash into a meaningful earnings-generating asset. A company holding $100 billion in Treasury securities can now earn around $4-5 billion annually with minimal risk.

This may not sound transformational at first, but the difference is enormous. During the zero-rate era, the same cash balance would have generated only a fraction of that amount. The opportunity cost of holding liquidity has fallen substantially, reducing the pressure on management teams to deploy capital immediately.

For the first time in years, patience pays.

Cash as a Strategic Asset

The growing cash hoard reflects more than financial conservatism. It represents a shift in how corporate leaders view liquidity.

Large cash reserves provide flexibility during economic downturns, protect companies against unexpected shocks, and allow management teams to act quickly when attractive opportunities emerge. Whether it is a market dislocation, a strategic acquisition, or a major investment initiative, companies with strong balance sheets possess options that highly leveraged competitors do not.

This strategic value becomes even more important in an uncertain economic environment where access to capital can become expensive or constrained.

The Death of Easy Acquisitions

For decades, acquisitions were one of the most effective ways for large corporations to deploy excess capital. Today, that option has become significantly more constrained, particularly for the world’s largest technology companies.

The reason is not simply that acquisitions have become expensive. Regulatory scrutiny has fundamentally changed the economics of dealmaking. Antitrust authorities in the United States, Europe, and the United Kingdom have become increasingly aggressive toward mergers involving dominant market players. Microsoft’s acquisition of Activision Blizzard faced a lengthy regulatory battle before ultimately receiving approval, while Alphabet continues to face multiple antitrust challenges across its core businesses.

This has created an unusual capital-allocation problem. Companies such as Microsoft and Alphabet continue to generate enormous amounts of cash, but many of the acquisitions that could meaningfully absorb that capital now face significant legal and regulatory hurdles.

As a result, capital that might once have been spent on transformative acquisitions is increasingly being redirected toward internal investment or simply retained on the balance sheet. For some of the world’s largest corporations, the era of easy acquisitions is effectively over.

The Investor Expectation Gap

Higher Treasury yields have undoubtedly made cash more attractive than it was during the zero-rate era. A company holding $100 billion in Treasury bills can now generate roughly $4-5 billion in annual interest income with minimal risk.

However, investors do not buy companies such as Apple, Microsoft, or Alphabet to earn Treasury-like returns. They invest in these businesses because they expect management to generate significantly higher returns through innovation, product development, acquisitions, and long-term capital allocation.

This creates a growing tension between management teams and shareholders. While executives value liquidity, flexibility, and downside protection, investors often view excessive cash balances as underutilized capital. Every dollar sitting in Treasury bills is a dollar that is not being deployed into opportunities that could potentially generate superior long-term returns.

The debate surrounding corporate cash reserves is therefore not about whether cash has value. It is about whether holding hundreds of billions of dollars in low-risk assets is the best use of capital for companies capable of generating much higher returns elsewhere.

When Companies Become Their Own Capital Markets

The implications of these cash reserves extend far beyond corporate balance sheets. When a handful of companies control more than $750 billion in liquidity, they gain a level of financial independence unavailable to most businesses.

Rather than relying on banks, bond markets, or venture capital investors, companies such as Apple, Microsoft, Alphabet, and Berkshire Hathaway can fund major strategic initiatives almost entirely through internal resources. This allows them to invest through downturns, pursue long-term projects, and absorb risks that smaller competitors often cannot afford.

In effect, the largest corporations are increasingly operating as self-funded economic ecosystems. While startups and smaller businesses face rising borrowing costs and tighter access to capital, cash-rich giants can finance multi-billion-dollar investments without seeking external funding.

The result is a growing concentration of financial power. The companies holding the largest cash reserves are not merely participants in the economy, they increasingly possess the balance-sheet strength to shape entire industries.

The Risk of Holding Too Much Cash

While large cash reserves provide flexibility, they are not always a positive signal. Excessive cash accumulation can sometimes indicate a lack of attractive investment opportunities, slowing growth prospects, or management’s inability to allocate capital effectively.

This challenge becomes particularly relevant for mature companies. Investors generally expect management teams to either reinvest capital at attractive returns or return excess funds to shareholders. When cash balances continue to grow without a clear plan for deployment, questions inevitably arise about whether that capital could be generating better returns elsewhere.

History offers several examples of companies that accumulated large cash reserves only to later pursue overpriced acquisitions or poorly timed investments. In such cases, the problem was not the cash itself but the pressure to eventually deploy it. Maintaining liquidity creates value only when management exercises discipline in deciding how and when to use it.

The key distinction, therefore, lies between strategic cash and idle cash. Strategic cash provides flexibility and optionality. Idle cash simply weighs on returns.

The Bigger Picture

The rise of corporate cash reserves reflects a broader shift in the global business environment. Economic uncertainty, geopolitical tensions, higher borrowing costs, and rapidly changing competitive landscapes have increased the value of financial flexibility.

At the same time, the largest corporations continue to generate extraordinary amounts of cash. Their profitability has reached a scale where even aggressive spending on capital expenditure, acquisitions, research and development, and shareholder returns often fails to fully absorb incoming cash flows.

As a result, balance-sheet strength has become an increasingly important competitive advantage. Companies with abundant liquidity can weather downturns more comfortably, seize opportunities more quickly, and avoid relying on expensive external financing when conditions deteriorate.

Conclusion

The great corporate cash hoard is not simply a story of cautious management teams refusing to spend money. It is the result of two powerful forces coming together: unprecedented cash generation by the world’s largest companies and a higher-interest-rate environment that has made liquidity far more valuable than it was during the zero-rate era.

Berkshire Hathaway, Apple, Alphabet, and Microsoft collectively hold more than $750 billion in cash and investments, yet these companies continue to spend heavily on growth, acquisitions, infrastructure, and shareholder returns. Their cash balances remain large not because they are avoiding investment, but because they generate capital faster than they can deploy it.

In today’s environment, cash is no longer a dormant balance-sheet asset. It generates meaningful income, provides protection against uncertainty, and gives companies the flexibility to act when opportunities arise. What was once viewed as a drag on returns has increasingly become a strategic asset, one that some of the world’s most successful companies appear unwilling to give up.

{kind=link}