Not every pharmaceutical company grows by discovering the next breakthrough drug.

Some create more value from the medicines they already have.

BioMarin Pharmaceutical is following that path, focusing on expanding existing blockbuster products, reaching new patients, making targeted acquisitions, and improving efficiency.

As drug development grows more expensive and risky, many biotech companies are finding that lasting growth comes from maximizing proven therapies rather than constantly launching new ones.

The question is whether this strategy can make BioMarin a durable long-term growth story.

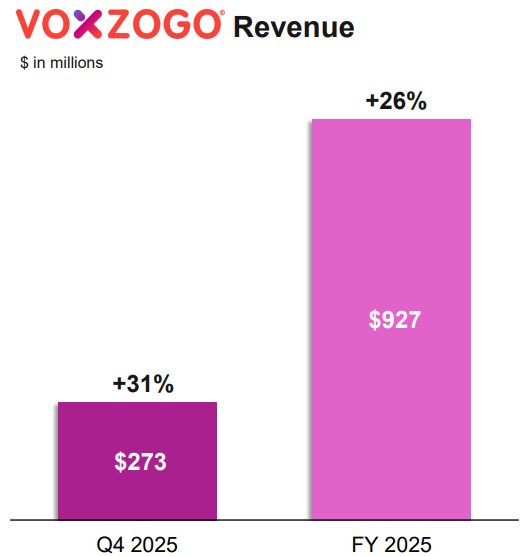

VOXZOGO Is Becoming BioMarin’s Biggest Growth Engine

If there is one product defining BioMarin’s future, it is VOXZOGO.

Originally developed to treat achondroplasia, the most common form of dwarfism, the therapy has rapidly become one of the biotech industry’s fastest-growing rare disease products. In 2025, VOXZOGO revenue increased by 26%, reaching nearly $927 million, while demand expanded across 55 commercial markets worldwide. Interestingly, about 73% of the drug’s sales now come from outside the United States, giving BioMarin substantial room for further global expansion.

But management is not stopping there.

The company is conducting late-stage studies for hypochondroplasia and is also advancing research into conditions such as idiopathic short stature, Turner syndrome, SHOX deficiency, and Noonan syndrome. Rather than spending billions to invent entirely new drugs, BioMarin is attempting to unlock new markets from an existing blockbuster.

This strategy reduces development risk while potentially creating multiple long-term revenue streams from a single asset.

Legacy Rare Disease Portfolio

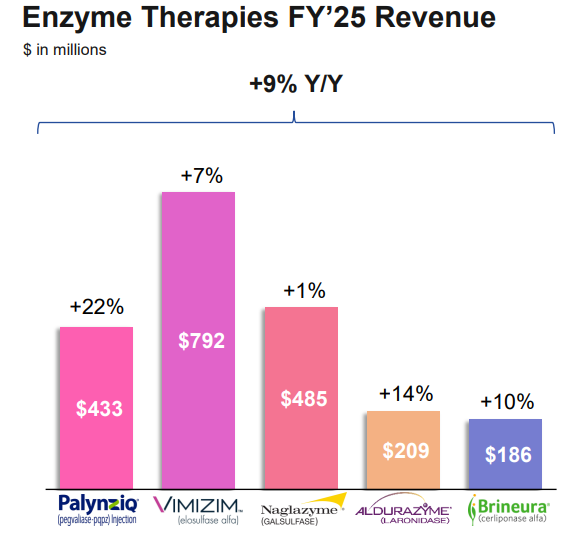

Many investors focus almost entirely on BioMarin’s pipeline, but the company’s established enzyme therapies remain the financial backbone of the business.

Products such as VIMIZIM, PALYNZIQ, BRINEURA, NAGLAZYME, and ALDURAZYME continue to enjoy high patient retention rates and relatively limited competition due to the specialized nature of rare disease treatments.

In 2025, BioMarin’s enzyme therapy portfolio delivered 9% revenue growth, while PALYNZIQ alone expanded by an impressive 22%. Together, these mature therapies generated more than $2.1 billion in annual revenue, providing the stable cash flows needed to fund research and future expansion.

Unlike many biotechnology companies that depend on one or two experimental products, BioMarin has built a diversified portfolio that compounds over time.

Expanding Existing Labels

Developing a completely new medicine can take well over a decade and often costs billions of dollars, with no guarantee of success.

BioMarin is increasingly choosing a different path by expanding approved therapies into broader patient populations.

The company expects regulatory decisions for PALYNZIQ’s adolescent expansion while simultaneously seeking broader approvals for VOXZOGO. This approach allows BioMarin to leverage existing manufacturing facilities, physician relationships, and commercial infrastructure without starting from scratch.

For shareholders, label expansions often produce some of the highest returns on investment in the pharmaceutical industry because development costs are lower while commercial execution is already established.

Amicus Acquisition

Organic growth is only one part of BioMarin’s strategy.

In late 2025, the company announced its acquisition of Amicus Therapeutics in a deal valued at approximately $4.8 billion. The transaction brings two established rare disease therapies into BioMarin’s portfolio: Galafold for Fabry disease and the Pompe disease treatment combination Pombiliti and Opfolda.

The acquisition immediately expands BioMarin’s presence in the rare metabolic disease market while creating opportunities to use its existing global commercial infrastructure to accelerate product sales.

Industry analysts believe the combination could become earnings accretive within the first year after closing, with even larger financial benefits expected beyond 2027.

Rather than diversifying into unrelated therapeutic areas, BioMarin is reinforcing the niche where it already possesses deep expertise.

Sometimes Growth Means Knowing What to Leave Behind

One of the more overlooked aspects of BioMarin’s strategy is its willingness to abandon projects that no longer make financial sense.

The company chose to voluntarily withdraw ROCTAVIAN, its gene therapy product, after commercial expectations failed to materialize. Although the decision resulted in accounting charges, management effectively redirected resources toward products with stronger long-term growth prospects.

In biotechnology, where companies often continue investing in struggling assets for years, this level of capital discipline can become a competitive advantage.

Profitability is Growing Alongside Revenue

Revenue growth alone does not create shareholder value.

BioMarin has also focused heavily on operational efficiency, generating approximately $828 million in operating cash flow during 2025 while ending the year with roughly $2 billion in cash and investments. The company expects operating margins to remain strong even as it integrates the Amicus acquisition.

This growing cash generation gives BioMarin the flexibility to invest in research, pursue acquisitions, and expand internationally without relying excessively on external financing.

Conclusion

BioMarin is not trying to become the biggest pharmaceutical company in the world.

Instead, it is attempting to become the dominant player in one of healthcare’s most profitable niches: rare genetic diseases.

Its strategy is surprisingly straightforward – expand blockbuster products, broaden patient populations, strengthen the existing portfolio through targeted acquisitions, and maintain financial discipline.

In an industry where fortunes often depend on a single clinical trial, BioMarin is building something far more predictable: a biotechnology business designed to compound over time.

That may ultimately prove to be its greatest competitive advantage.

{kind=link}